One strategy that consistently captures the attention of investors is the carry trade. Traditionally associated with currency trading, the carry trade can also be applied to the fixed income market, specifically through short-term government securities like 3-month Treasury bills (T-bills). The essence of this strategy lies in capitalizing on interest rate differentials between countries, borrowing in low-interest-rate environments, and investing in higher-yielding assets. However, the recent developments in global markets -particularly the yen carry trade unwind – underscore the risks involved in this seemingly straightforward strategy.

This article explores the historical performance of 3-month T-bills across various countries, providing a comparative analysis that highlights the opportunities and risks inherent in the global carry trade. We’ll explore the dynamics of the US T-bill market, examine the impact of foreign exchange (FX) movements on returns, and dissect the implications of the yen carry trade unwind.

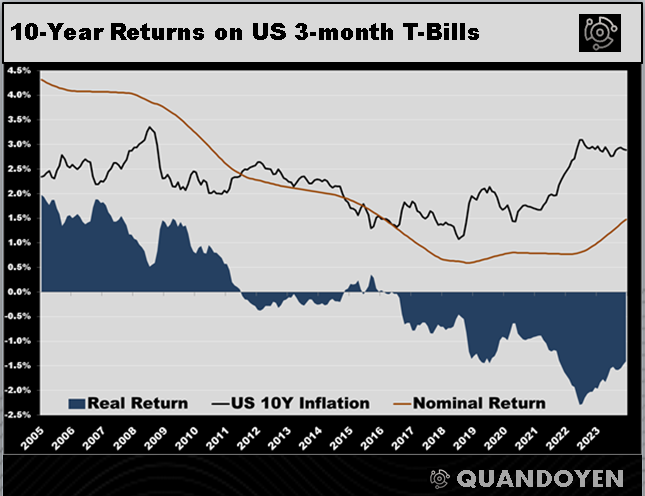

1. US 3-month T-Bill Returns: A Historical Perspective

The performance of US 3-month T-bills has been anything but static over the past few decades. From the mid-2000s to the mid-2010s, nominal returns on these securities were on a downward trajectory, largely due to the Federal Reserve’s ultra-loose monetary policy in response to the 2008 financial crisis. With interest rates at or near zero, the appeal of T-bills as an investment was diminished, especially when inflation was factored in. Real returns, which adjust for inflation, often dipped into negative territory during this period, challenging the traditional notion of T-bills as a “safe” investment.

However, the landscape began to shift in 2021 as inflationary pressures mounted. The confluence of supply chain disruptions, expansive fiscal policies, and a post-pandemic economic recovery led to a surge in inflation, prompting the Federal Reserve to adopt a more hawkish stance. As interest rates rose in response, so too did the yields on T-bills. This environment enhanced the appeal of USD-denominated assets, driving capital inflows into the US and contributing to the strengthening of the dollar.

Despite this resurgence, the key takeaway for investors is the necessity of a dynamic approach. Relying solely on US T-bills – particularly in periods of low or negative real returns – can be suboptimal. Diversifying into T-bills from other countries with different interest rate cycles offers the potential for better returns, especially when US yields are low.

The rest of this article is available on Medium and Linkedin